Presented to International Copper Study Group on Spring 2002 Meeting in Santiago, Chile

March 22, 2002

This paper examines opportunities and threats facing the North American copper market, focusing on the top six markets, which combined account for almost two-thirds of consumption.

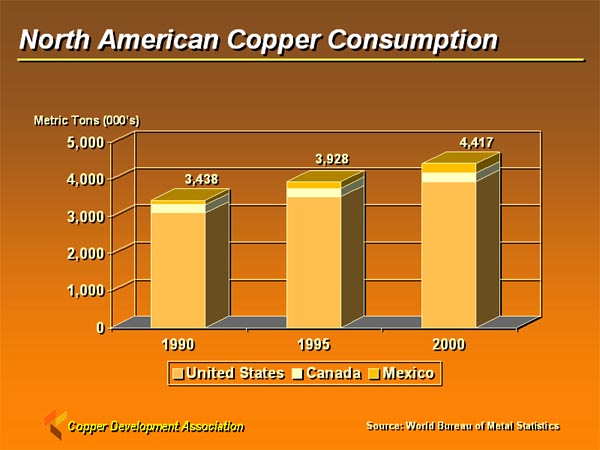

Over the past eleven years North American copper consumption has increased by almost one million tonnes, from 3,438,000 tonnes in 1990 to 4,417,000 in 2000. North America consumes 24 percent of the world's copper, with the United States accounting for 21½ percent of copper consumption and Mexico and Canada 1.4 and 1.2 percent respectively.

North American Copper Consumption Slide

{kind=link}

Building Wire

Building wiring, the largest market, accounted for 16.8 percent of consumption in 2000. This translates into over 740,000 tonnes of copper. Copper is the material of choice, by far in the building wiring market with a 92 percent share in 2000. Copper's dominance in this market is a testimony to its many strengths. Copper, by virtue of its inherent high conductivity, ductility and strength, has always been the ideal material for conducting electricity.

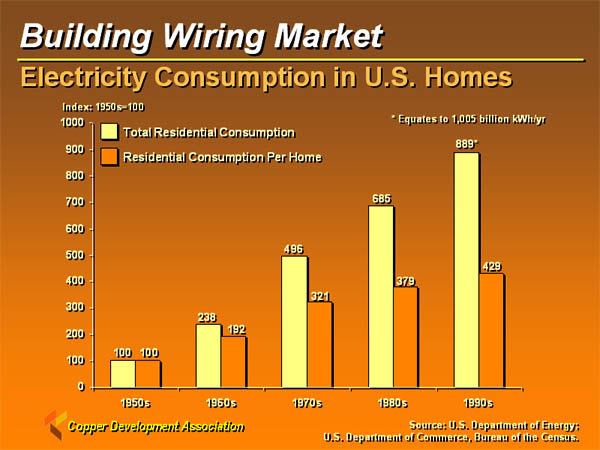

Copper building wire has benefited from the increase in residential energy consumption. Let's take the U.S. market as an example. In the 1950s US residences consumed 113 billion kWh in an average year, by the 1990s consumption was nearly nine times as much. On an index basis that's an increase from 100 to 889 for that 40-year period. Even when factoring the growth in the number of homes over this period of time, consumption of electricity still quadrupled. But homes in the 1950s didn't have all the electrical apparatuses that they do today. And yet the average home today in the US doesn't have four times as much current-carrying capacity as the typical home in the 1950s. One can therefore make the argument that home wiring hasn't kept pace with demand.

Electricity Consumption in US Homes Slide

{kind=link}

This presents an opportunity for the copper industry. The upgrading of wiring in every room in a house from AWG 14 to AWG 12 gage, so that it can handle a heavy electrical load if needed. All rooms should be supplied with adequate capacity, both in terms of number of circuits, and numbers of outlets. It's a matter of wiring homes so they meet not only today's electrical needs, but also the electrical needs of tomorrow.

Another opportunity for copper usage in this market is an area referred to as power quality in commercial and industrial buildings. This refers to the proper wiring and grounding of buildings and structures to solve power quality problems, such as harmonics and transients. Many of these problems, caused in large part by the proliferation of computers and other electronic equipment, can be solved by the use of heavier gage wire in power legs and neutrals, proper grounding procedures, both inside and outside the building, including adequate lightning protection, use of fewer outlets per circuit, and proper equipment. A Copper Development Association market study determined that there is an opportunity to use as much as 20 - 40 percent more copper wiring simply because of power quality considerations.

Plumbing & Heating Market

Copper's second largest market, plumbing & heating, consumed over 570,000 tonnes in 2000. Its usage is almost evenly divided between residential and non-residential applications. In residential applications the greatest usage of copper is for water distribution. It is here that copper also has the greatest market share of any of its applications in the plumbing & heating market.

In nonresidential applications a Copper Development Association market study showed copper's greatest usage to be in retail/restaurant buildings. It should be noted however, that this study was based on a limited sample and information on additional buildings is being gathered on an on-going basis.

Despite copper's many strengths, it faces strong competition from competitive materials in the plumbing & heating market. Plastic tube and pipe continue to be the main competition in water service, distribution and drainage. Steel and plastic are strong in fire sprinklers, fuel and fuel gas distribution systems and mechanical systems.

But the copper industry, through the North American copper centers, is aggressively defending copper's position in this important market. Promotional literature extolling copper's many benefits targets builders and consumers. An extensive training program is successfully teaching plumbers how to install copper tube and pipe. Copper is being promoted for fuel-gas distribution systems to builders, plumbers, utilities and related trade associations through technical literature and the Copper Development Associations piping and fuel-gas websites. These are just a few of the many ongoing activities to promote and defend copper in the plumbing & heating market.

Automotive Market

The automotive market is undergoing a number of technological changes. The Patent & License Exchange published in October 2001 the top ten automotive technology markets. Five out of the top ten have important implications for copper. These technology markets are providing opportunities for copper in such areas as, 42-volt systems, hybrid vehicles and a myriad of electrical and electronic applications.

Top 10 Automotive Technologies Slide

{kind=link}

Over the years, more and more electrical and electronic content has been added to the automobile creating the need for growth in the power and signal distribution system, also known as the wiring harness. Historically electrical content in the automobile has grown at a rate of about 4 percent, causing similar growth in the mass of the wiring harness. More recently, that growth has increased to about 10 percent. With the ever-increasing electrical/electronic content in the automobile, the power required is fast approaching the limit of today's 14-volt system. The current power generation system is capped at 1800 watts. According to industry sources, it is predicted that energy demand could reach as high as 3,000 to 7,500 watts by 2005. This will drive the automotive industry to 42-volt systems. This transition is not expected to be an easy one for manufacturers. They are still grappling with the type of architecture to use. Most manufacturers are working on a dual-volt system. Many of the electrical components found on the vehicle will have to be redesigned to work effectively with higher voltage systems. This is an expensive process and most manufacturers will elect to make the transition on a model-by-model basis as they go through the normal upgrading of the model.

Applications Increasing Electronic Content Slide

{kind=link}

The move toward higher voltage vehicles will affect copper content in the vehicle. While some components will experience a decrease in copper content, as more power becomes available, new electrical components and systems will emerge. While no one knows exactly what the net affect will be for the copper industry, our analysis shows the increases should outweigh the decreases and result in an increase in copper content for the vehicle.

While many systems, such as electronic valve actuation, electric HVAC, and electric braking, have the potential to add several kilograms of copper to the vehicle, these systems are not expected to enter the vehicle fleet in significant numbers until after 2010. While there is little doubt within the automotive industry that higher voltage vehicles will emerge over the next ten years, arcing and cost are great hurdles that must be overcome for these systems to become available on a mass scale.

One area already increasing copper content and a reality today is hybrid vehicles. These vehicles utilize a battery and an internal combustion engine to power the vehicle. While there are a number of battery technologies competing for use on hybrid vehicles, nickel metal hybrid is the leading technology. NiMH batteries dominate the hybrid electric vehicle and electric vehicle markets due to performance, cost, safety and flexible packaging. Texaco Ovonic the manufacturer of NiMH batteries estimates that there are 96 pounds of copper in each battery. Today, all commercially available hybrid electric vehicles are powered by NiMH batteries, including the GM Precept, Toyota Prius and the Honda Insight.

This does not take into account the potential for these batteries in electric vehicles and heavy-duty vehicles. Virtually all commercial electric vehicles, which are listed on this slide, are powered by these batteries.

Power Utilities

Now let's take a look at the power utilities market. This market, which consumed over 360,000 tonnes of copper in 2000 is benefiting from the drive toward more energy efficient motors and transformer. Industry and government associations are actively working to promote the utilization of more efficient motors and transformers. And copper's strength in conductivity is helping it to capture a larger and larger share.

In addition more energy efficient motors and transformers utilize more copper. There is an incremental potential of an additional 20,000 tonnes of copper due to energy efficiency. Now let's listen to David Brender, Copper Development Associations National Program Manager for Electrical Energy Efficiency talk about the benefits of this program to copper.

Air Conditioning & Refrigeration

Another important market to the copper industry is air conditioning and refrigeration, which consumed over 360,000 tonnes of copper in 2000. Copper, with its many strengths, has a strong position in this market, But there is room for increases in unit usage due to the drive for increased energy efficiency in air conditioning and refrigeration products. The Copper Development Association is co-funding research with the Air Conditioning & Refrigeration Institute to find new ways to increase energy efficiency.

Telecommunications

Telecommunications is a dynamic market undergoing a number of changes. Copper consumption peaked in this market in the late 70s, reached a low in the early 90s and has been climbing back since then.

DSL is today's technology for copper in the telecommunications market. This and premises wiring are two key opportunities for copper. DSL stands for Digital Subscriber Line. It is a dedicated circuit from your home to the telephone company's central office, utilizing normal copper telephone lines. It has a number of advantages. The downstream speed of DSL gives the user the ability to download files considerably faster that other technologies as evidenced here. It is three times faster than an ISDN line and almost 15 times faster than an analog dial-up connection.

Another opportunity in this market for copper, premises wiring also referred to as structured wiring. Structured wiring while already established in the commercial sector, is a dynamic growing market in residential construction. But first, what exactly is structured wiring. For the residence it is a system for phone, data and television wiring that consists of a method of interconnecting rooms of the house according to accepted standards.

This year it is estimated that almost 30 percent of the homes built will be wired with structured wiring. The new homes market is the quickest and easiest to penetrate because the walls are open, making it easy to wire. Estimates indicate that a properly wired home contains approximately 9 kilograms of copper structured wire. At a 30 percent penetration, that equates to 450,000 homes with structured wiring.

And that doesn't even take into account the retrofit market. In the United States alone, there are around 106 million homes that potentially can be retrofitted with structured wiring. While retrofitting homes is more difficult than new homes, it is not impossible to do so. It is unlikely that this segment of the market will ever achieve the penetration rates in new construction. However, to equal the same number of homes as in new construction requires a penetration of less than one percent. This exciting dynamic market has great potential for the copper industry.